Despite having been developed almost a century ago, automated shading products are currently installed on only a few percent of windows in the U.S. In contrast, automatic washing machines—which were developed at about the same time—had reached about 60% of U.S. homes with electricity by 1940, and about 80% of all U.S. homes by the mid-1980's.

The reason for this disparity seems obvious: most buyers of home appliances and furnishings are value-conscious. And washing machines are generally regarded as cost-effective labor-saving appliances, while automated shading is considered a luxury.

On the other hand, washing machines were also considered luxuries when they were first introduced. If automated shading could somehow make the same transition from luxury to cost-effective appliance, sales would grow by an order of magnitude, exceeding $2B per year in the U.S. alone.

But to do that, automated shading products must offer mainstream buyers a compelling value proposition—and that's something that conventional automated shading technology just can't do.

The Key Market Segments

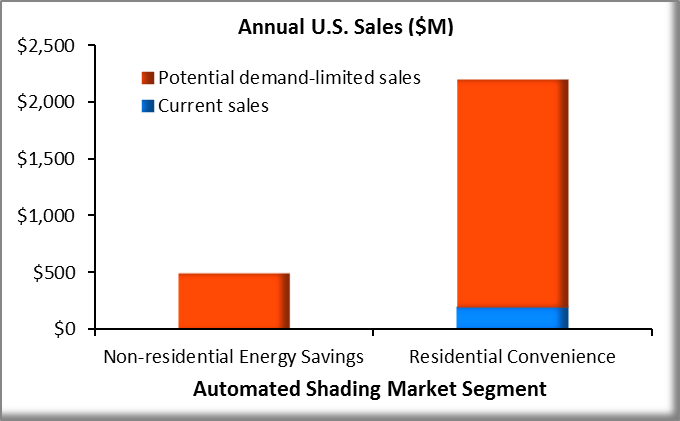

Automated shading offers a variety of potential benefits, including convenience, enhanced aesthetics, privacy, security, prestige, and energy savings. But only two of those benefits represent compelling value to mainstream buyers: convenience in residential buildings, and energy savings in office buildings.

Achieving substantial market penetration in these two key segments depends on providing enough of those benefits at a low enough price. That's not currently happening, so the segments remain virtually untapped:

In addition to remaining virtually untapped, the two key segments have something else in common: demand is highly correlated with perceived value—and perceived value in each segment can be quantified as a function of product characteristics.

Energy-Saving Retrofits for Office Buildings

Buildings account for 40% of all the energy consumed in the U.S., and many existing buildings are still equipped with relatively inefficient HVAC and lighting systems. As a result, there is a thriving market for energy saving products and services for existing non-residential buildings, with annual sales exceeding $10B in the U.S. alone.

Automated window shading is a potential player in this market segment for two reasons: it can minimize the thermal loads on a building's HVAC system, and (more significantly) it can maximize glare-free daylight which can then be "harvested" in the form of energy savings by automatically dimming the lamps.

The savings from daylight harvesting are especially impressive in office buildings, because they're occupied mostly in daytime and have relatively high energy intensities and window-to-wall-area ratios. Using a high-performance automated shading system with a daylight-harvesting lighting control in a typical windowed office space can save over 50% of the energy consumed in lighting, with over 50% of those savings attributable to automated shading.

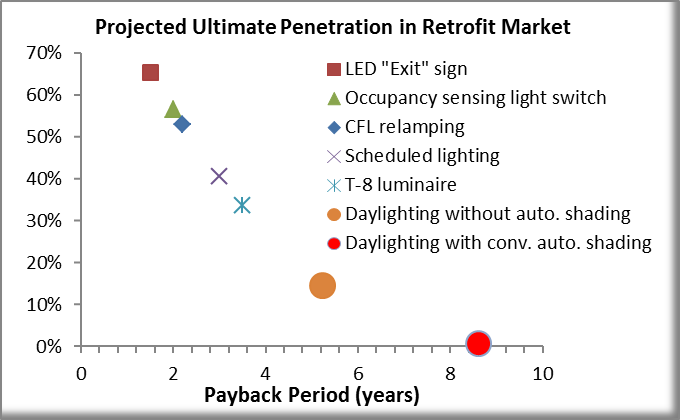

The Payback Period

Unfortunately, impressive energy savings aren't enough to guarantee market success. Instead, it's the payback period, defined as the ratio of installed price to annual dollar savings, that determines ultimate market penetration. Energy saving products that have payback periods of less than a few years achieve high market penetration, while penetration drops to near zero for paybacks longer than six years or so (despite the fact that a six-year payback would be considered excellent for other types of investment).

And that's the issue with conventional automated shading technology: despite its impressive energy saving potential, it's so expensive that it lengthens the payback period for daylight harvesting, pushing it to well beyond what the market is willing to accept.

As a result, the market penetration of automated shading in the energy efficient retrofit market is effectively zero—and will remain so until the payback period drops substantially (or the market becomes more payback-tolerant):

As the chart shows , the payback period of conventional automated shading technology would have to be slashed by at least 50% in order to achieve significant market penetration. While that's a daunting challenge, the potential payoff is huge: the market is hungry for new energy saving technologies that meet the market's stringent payback criteria.

Enhancing Convenience in Residential Buildings

Automated shading can't save as much energy in residential buildings as in non-residential buildings, because lighting power densities are lower and average building occupancy doesn't peak until after the sun goes down.

But automated shading does offer a benefit that's more compelling in residential buildings than in non-residential buildings: convenience. People adjust window shading more often in residential buildings than in non-residential buildings, so automated shading saves more time and effort. And the people who specify improvements to non-residential buildings don't care nearly as much about tenant convenience as the people who buy appliances and furnishings for their own homes.

The Price-to-Convenience Ratio

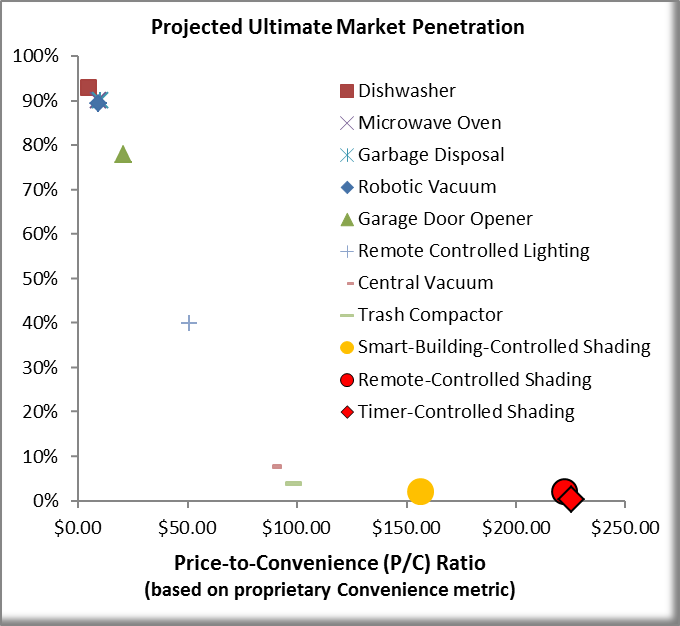

But how much are residential buyers willing to pay for added convenience? Unlike the market for non-residential energy saving upgrades, the market for residential convenience-enhancing products doesn't have a generally accepted value metric.

However, that doesn't mean that value can't be quantified. In fact, we've found a way to quantify the convenience provided by any labor-saving product, and have been able to use it to verify that ultimate market penetration varies linearly with the inverse of what we call the Price-to-Convenience (P/C) ratio:

Of course, individual buyers don't consciously quantify a product's P/C ratio. Instead, a shared awareness of its cost-effectiveness emerges as it diffuses into the market, gradually influencing buyers' attitudes toward it:

- Products with P/C ratios lower than a specific threshold (about $100/C in the relative units of Chart 3) are eventually regarded as useful appliances by mainstream buyers, and the demand for them is elastic with their P/C ratios.

- On the other hand, products with P/C ratios higher than the threshold are viewed as luxury or prestige items and achieve only limited penetration. Demand for these products is only weakly correlated with the P/C ratio, so the best product-improvement strategy is often to focus on aesthetics and exclusivity rather than affordability or functionality. But while that strategy can increase market penetration in niche segments, it usually moves the product even further off the playing field in the mainstream value-driven segment.

Obviously, conventional automated shading products fall into the second category. The challenge for automated shading is that opening and closing window coverings by hand requires much less cognitive and physical effort than the tasks automated by other labor-saving appliances (e.g. automatic dishwashers). So, since they save much less effort, automated shading products must also cost much less than the other appliances in order to provide a competitive P/C ratio. In fact, as Chart 3 shows, the costs of conventional automated shading products would have to decrease by at least 50%—with no compromise in functionality—in order to be considered mainstream labor-saving appliances.

Out of the Niche and Into the Mainstream

Is there any guarantee that reducing a niche product's P/C ratio to below the threshold will turn it into a mainstream appliance? No, but there's certainly plenty of precedent for that to happen. For example, the most successful products on Chart 3 (dishwashers and microwave ovens) had P/C ratios comparable to today's automated shading products when they first entered the market, and were considered luxury products that would never break into the mainstream.

A more recent (and relevant) example is the Roomba® robotic vacuum cleaner developed by iRobot®. iRobot® wasn't the first to attempt to develop a mainstream robotic vacuum-cleaning appliance; in fact, the first such efforts predated the Roomba® by almost two decades. However, earlier efforts were aimed at maximizing capability (with the aim of completely replacing conventional vacuum cleaners), rather than maximizing cost-effectiveness. iRobot® was the first to recognize that the key to bringing robotics to the mainstream market was to offer a product that's at least as cost-effective as conventional labor-saving appliances.

The success of the Roomba® surprised some people, but as Chart 3 shows, it shouldn't have. While it doesn't completely eliminate the need for occasional manual vacuuming, it does save enough labor at a low enough price to offer compelling value to mainstream buyers. That's why it (and other products in the category it pioneered) are on-track to achieve the high market penetration predicted by our P/C model.

Where Conventional Automated Shading Products Are Headed

So what are people doing to make automated shading more market-friendly? Some are focusing on the shading device itself, attempting to perfect a solid-state "smart glazing" technology that would eliminate the need for movable window coverings entirely. But while that would make automated shading more elegant, it wouldn't make it smarter or easier to use. And even after decades of investment, smart glazing technology is still an order of magnitude too expensive for mainstream architectural use—and seems destined to remain so for the foreseeable future.

So, most of the R&D in automated shading isn't aimed at the shading device per se, but rather at bringing motorized window coverings into the "Internet of Things" (IoT) by giving them connectivity and writing apps to control them remotely. But web-enabling a product doesn't necessarily make it more affordable, smarter, or easier to use. So, while everything may eventually be connected to the internet, internet connectivity alone won't be enough to turn a niche automated shading product into a mainstream one.

In recognition of that fact, still others are writing "smart building" apps that can turn a group of devices on the IoT into an intelligent building ecosystem. That will certainly make building systems smarter, but it won't make them cheaper—and it won't provide much benefit until a critical mass of devices is on the IoT, which could take years. And for many of these apps (particularly for residential use), the smartness depends on user-defined if/when-then rules, which makes them harder to use and less appealing to potential mainstream buyers.

So is there any way to exploit the market gap in the near-term, after all? Absolutely.

Offering a Compelling Value Proposition

Nobody familiar with the automated shading market would need the data of Charts 2 and 3 to know that conventional products don't offer compelling value to mainstream buyers. But Charts 2 and 3 quantify the problem, indicating exactly how (and by how much) automated shading has to evolve in order to penetrate the mainstream market.

Obviously, however, just knowing the extent of a problem doesn't ensure a solution. In fact, it took years of effort and multiple innovations to develop an automated shading technology with the cost-effectiveness necessary to succeed in the mainstream market.

And finally, it's here: patented IntelliShading™ Technology.